Urban Kenyas Growing Trust In Saccos: A Call To Strengthen Cooperative Finance Nationwide

By Admin Thursday, 26th March 2026

Photo courtesy

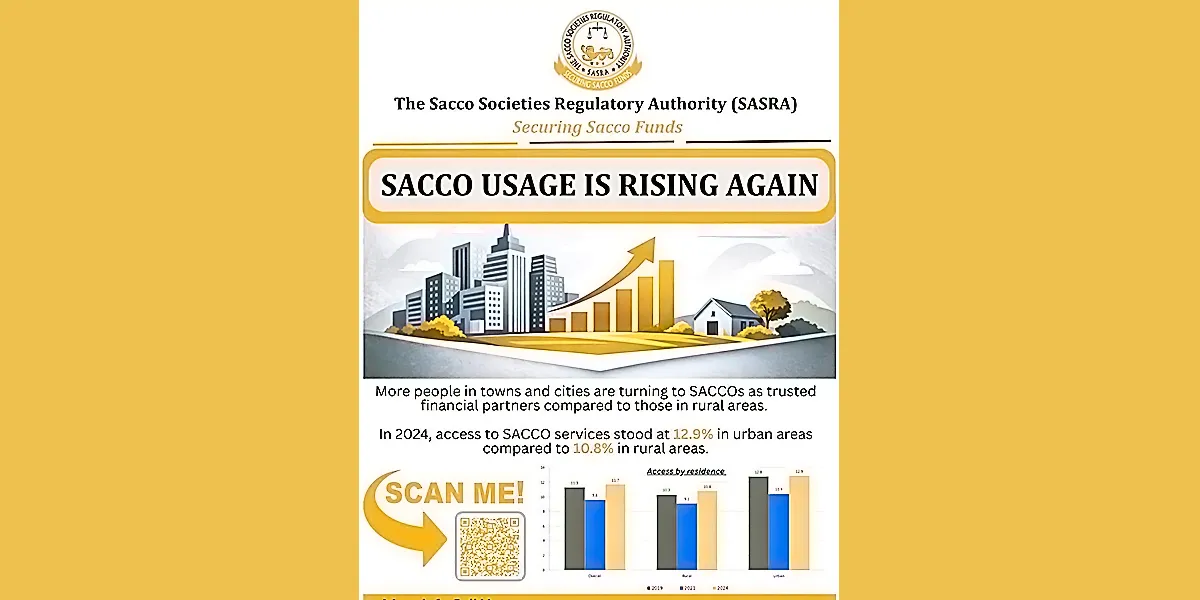

The release of the FinAccess Household Survey 2024 Report has once again highlighted the evolving dynamics of financial inclusion in Kenya. Notably, the report reveals that more people in urban areas are increasingly turning to Savings and Credit Cooperative Organizations (SACCOs) as trusted financial partners compared to their rural counterparts. In 2024, access to SACCO services stood at 12.9% in urban areas, compared to 10.8% in rural areas.

This emerging trend is both encouraging and thought-provoking. For decades, SACCOs have been deeply rooted in rural communities, serving as critical financial lifelines for farmers, small traders, and informal sector workers. The growing uptake in urban centers signals not only a shift in perception but also an expansion of the cooperative model into new and dynamic economic spaces.

As the apex body representing the cooperative movement in Kenya, the Cooperative Alliance of Kenya (CAK) views this development as a significant milestone—while also recognizing the urgent need to bridge the rural-urban gap and ensure that cooperative finance remains inclusive, accessible, and impactful for all.

The Rising Appeal of SACCOs in Urban Areas

Urban Kenya is characterized by a fast-paced economy, diverse income streams, and a growing middle class. In such an environment, individuals and businesses are constantly seeking financial solutions that are flexible, affordable, and trustworthy. SACCOs have increasingly positioned themselves to meet these needs.

Unlike traditional financial institutions, SACCOs are member-owned and driven by the principle of mutual benefit. This unique structure fosters trust, transparency, and a sense of ownership among members. For many urban dwellers—especially salaried employees, small business owners, and gig workers—SACCOs offer an attractive alternative to commercial banks.

Key factors driving urban adoption include competitive interest rates on loans, higher returns on savings, personalized services, and the ability to access credit based on one’s savings history rather than rigid collateral requirements. Additionally, the digitization of SACCO services has made it easier for urban members to transact, monitor accounts, and access financial products conveniently.

The rise in urban SACCO membership also reflects a broader shift in financial behavior. As the cost of living continues to rise in cities, individuals are becoming more intentional about saving, borrowing responsibly, and investing in their financial future. SACCOs, with their community-oriented approach, are well-positioned to support this shift.

Why Rural Access Still Matters

While the growth in urban SACCO access is commendable, the lower uptake in rural areas raises important questions. Rural communities remain the backbone of Kenya’s agricultural sector and are home to a significant portion of the population. Ensuring that these communities have access to strong and effective SACCOs is essential for equitable development.

Several factors may contribute to the relatively lower rural access. These include limited awareness of SACCO products and services, weaker institutional capacity of some rural SACCOs, and infrastructural challenges such as poor connectivity and limited access to digital platforms. In some cases, governance issues and lack of trust may also hinder participation.

It is important to note that many rural SACCOs have historically played a transformative role in improving livelihoods. From financing agricultural inputs to supporting education and housing, these institutions have been central to rural economic empowerment. Strengthening them is not just a financial imperative—it is a development priority.

Bridging the Gap Through Stronger Cooperatives

The disparity between urban and rural SACCO access underscores the need for targeted interventions aimed at strengthening cooperative institutions across the country. For CAK, this aligns directly with our mandate of advocating for a vibrant, inclusive, and sustainable cooperative movement.

Capacity building is a critical starting point. Rural SACCOs must be supported to improve governance, enhance financial management, and adopt best practices. This includes training for board members, management teams, and members to ensure that cooperatives are run professionally and transparently.

Digitization is another key enabler. Expanding access to mobile and digital financial services can significantly improve the reach and efficiency of SACCOs in rural areas. By leveraging technology, SACCOs can overcome geographical barriers and provide members with convenient access to services.

Furthermore, there is a need for increased awareness and financial literacy. Many potential members may not fully understand the benefits of joining a SACCO or how to participate effectively. Public education campaigns, supported by government and stakeholders, can help demystify SACCO operations and encourage greater participation.

The Role of Policy and Regulation

A supportive policy and regulatory environment is essential for the growth of SACCOs. Institutions such as the Sacco Societies Regulatory Authority continue to play a vital role in ensuring that SACCOs operate within a framework that promotes stability, accountability, and member protection.

Regulation must strike a balance between safeguarding members’ interests and enabling innovation. As SACCOs expand into urban markets and adopt new technologies, regulatory frameworks must evolve to address emerging risks while supporting growth.

At the same time, policies should encourage the establishment and strengthening of SACCOs in underserved areas. Incentives, partnerships, and targeted programmes can help drive investment into rural cooperative finance and ensure that no community is left behind.

Leveraging Urban Growth for National Impact

The increasing popularity of SACCOs in urban areas presents an opportunity to strengthen the entire cooperative ecosystem. Urban SACCOs often have access to larger capital bases, more diverse membership, and greater exposure to innovation. These strengths can be leveraged to support rural SACCOs through partnerships, knowledge sharing, and resource mobilization.

For instance, successful urban SACCOs can mentor emerging rural cooperatives, share best practices, and even collaborate on joint projects. Such linkages can enhance the resilience and sustainability of the cooperative movement as a whole.

Additionally, the growth of urban SACCOs can contribute to national economic development by mobilizing savings, facilitating investment, and supporting entrepreneurship. As more people join SACCOs, the collective financial power of the cooperative sector increases, creating opportunities for large-scale impact.

CAK’s Commitment to an Inclusive Cooperative Movement

At the Cooperative Alliance of Kenya, our commitment is to ensure that the benefits of cooperative finance are accessible to all Kenyans, regardless of their location. The insights from the FinAccess Household Survey 2024 provide valuable guidance on where efforts should be focused.

We will continue to advocate for policies that strengthen SACCOs, promote inclusivity, and enhance member value. Our work in networking and partnerships will aim to connect stakeholders across the cooperative ecosystem, fostering collaboration and innovation.

We also recognize the importance of research and data in informing decision-making. By leveraging insights from reports such as the FinAccess Survey, we can better understand trends, identify gaps, and design interventions that are responsive to the needs of members.

Conclusion

The growing trust in SACCOs among urban populations is a positive sign for the cooperative movement in Kenya. It reflects the relevance and adaptability of the SACCO model in a changing economic landscape. However, the journey toward full financial inclusion is far from complete.

Bridging the gap between urban and rural access must be a priority. By strengthening cooperative institutions, investing in capacity building, embracing technology, and fostering inclusive policies, we can ensure that SACCOs continue to serve as engines of economic empowerment for all Kenyans.

As CAK, we remain committed to championing a cooperative movement that is strong, inclusive, and impactful—one that truly leaves no one behind.